There’s no open market to buy green credits in India. Here’s how compliance-driven companies actually access them in 2025 — and what to check first.

Written by Punnia Viswan | Co-Founder & CEO, Edha Sustainability Solutions LLP | Last updated: 4th July 2026 | All external links verified at the time of publication

Can you buy green credits in India?

If your plan for the year was to buy a tranche of green credits and retire them against a compliance obligation, we should start with an uncomfortable correction: that market doesn’t exist.

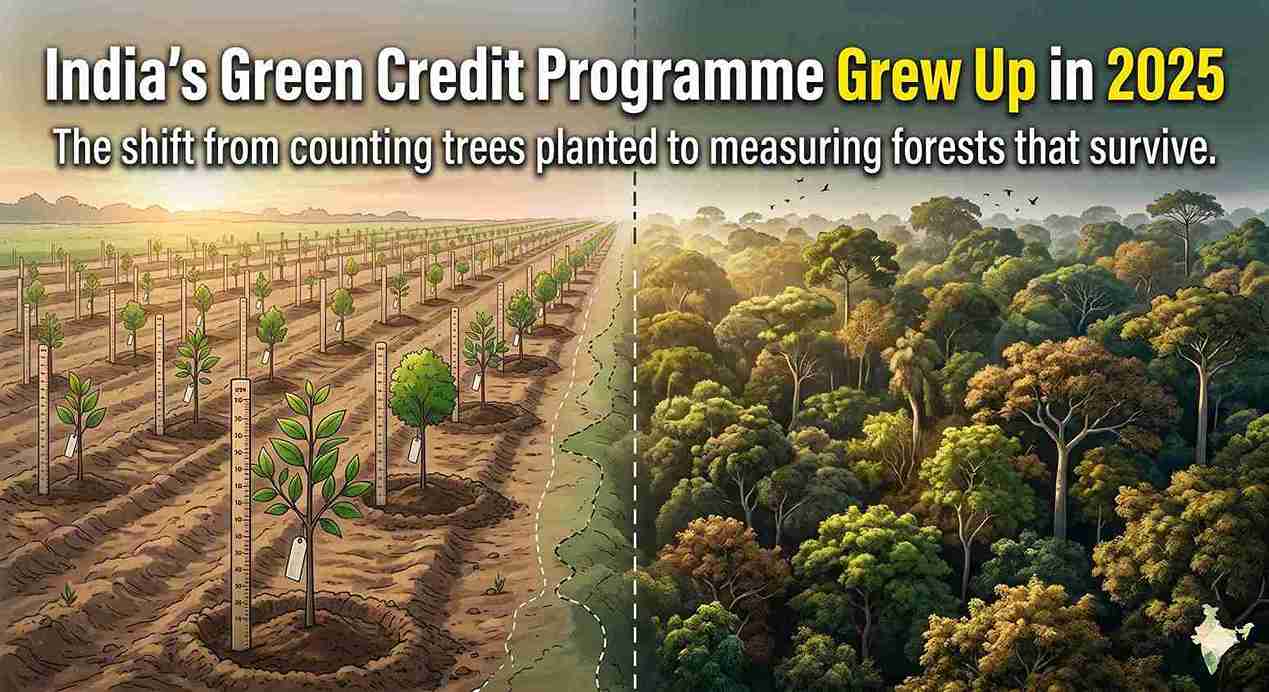

Under the revised Green Credit Rules, there is no open exchange where a company purchases green credits from a third party. The 2025 reforms made them non-tradable and non-transferable, with one narrow exception, and usable only once before they are extinguished. For a sustainability or CSR lead who has been told green credits are a flexible compliance instrument, that single fact reshapes the whole decision.

Key takeaways

- There is no open market for green credits in India — they are non-tradable, single-use, and extinguished on exchange.

- The realistic route for most companies is to fund a restoration project as the registered applicant: a ten-year commitment, not a CSR campaign.

- Compensatory afforestation is the sharpest reason to engage, but the exchange is not one-to-one — restored land must be two to four times the area being diverted (four times for most private projects), on top of a 25-hectare cumulative minimum and a ten-year maintenance liability.

- Credits issue only after five years and 40% canopy density, at one credit per surviving tree, so survival risk is capital risk.

- Confirm which offset multiplier (2×–4×) applies to your project type, and know what else is being claimed on the land, before you commit.

| What companies often assume | The 2025 reality |

| Green credits can be bought on an open market | Non-tradable and non-transferable, except holding ↔ direct subsidiary |

| A credit is a reusable compliance asset | Single-use — extinguished once exchanged |

| It’s a CSR-style annual spend | A 10-year commitment: 5-year establishment + 5-year maintenance |

| You buy credits, then retire them | You fund a project as applicant; credits issue only after 5 yrs + 40% canopy |

| Funding the project gives you the land | The tripartite MoU grants no ownership, lease, or resource rights |

| Green credits offset compensatory afforestation one-to-one | Restored land must be 2×–4× the diverted area, scaled by project type |

How do companies actually get green credits?

There are only two ways a company ends up holding them.

- Generate them by funding a project. You become the registered applicant behind a multi-year restoration project on degraded forest land, and credits are issued to you once the project performs.

- Receive them inside your own group. A holding company can pass credits to a direct subsidiary, or a subsidiary to its holding company. That is the only permitted transfer.

For most companies, that means route one. And it forces a reframe worth sitting with: a green credit is not a product you buy. It is the outcome of a project you commit to. That changes who needs to be in the room — finance and legal, not just the sustainability function.

Treat it as a capital commitment, not a CSR campaign

Funding a green credit project is a decade-long undertaking. The headline numbers:

- A ten-year horizon. A five-year establishment phase that you fund and execute, then a further five years of maintenance.

- Costs well beyond the planting. A 10% administrative fee on total project cost (split between the central administrator and the state forest department), a verification fee before credits are issued, and a maintenance deposit covering years six to ten. Inflation indexing needs to be built into the model from the start.

- No land tenure. The tripartite MoU grants no ownership, no lease, and no resource rights. The land and everything growing on it stays with the State Forest Department. You are funding restoration on land you will never control.

- Credits only if the trees live. Credits are issued after the five-year period and once the site reaches 40% canopy density, at one credit per surviving tree older than five years. No survival, no credit.

- Single use. Once you exchange a credit against an obligation, it is gone. There is no second life and no resale.

Is a green credit project a CSR spend or a capital commitment?

Compensatory afforestation is the sharpest reason to engage. On 15 September 2025, MoEFCC issued guidelines (OM No. FC-11/104/2025) under the Van (Sanrakshan Evam Samvardhan) Amendment Rules, 2025, allowing afforestation raised over degraded forest land under the Green Credit Programme to be exchanged toward compensatory afforestation — the statutory replanting a company owes when it diverts forest land for a project. Unlike CSR or disclosure, this is a hard obligation with a real budget line, which is why it anchors the business case.

But the exchange is not one-to-one, and that is the detail most companies miss. Restored land does not offset diverted land acre-for-acre. The guidelines require the restored area to be a multiple of the land being diverted, scaled by project type — and for the residual category that captures most private diversions, that multiple is four times the diverted area.

| Project category | Restored land required |

| Central government, CPSU, transmission-line, and critical & strategic mineral / atomic-substance projects | 2× |

| Projects in states/UTs with over 33% forest cover (with a non-availability certificate) | 2× |

| Certain non-critical mining minerals in less-forested states | 3× |

| All other projects — the residual category most private diversions fall into | 4× |

On top of the multiplier, the preconditions are specific. To exchange restored land this way:

- each parcel must be a minimum of five hectares, restored for at least five years, at 40% canopy density, and already awarded green credits;

- the user agency must have cumulatively restored at least 25 hectares of degraded forest land;

- the land must be free of all encumbrances and demarcated at the applicant’s cost; and

- the user agency carries maintenance and protection for ten years.

And one hard limit: site-specific plantation obligations cannot be met through green credits at all. So the due-diligence task here is to confirm which multiplier applies to your project category — the gap between 2× and 4× restored land changes the economics entirely, and it is the difference between this route being viable and being prohibitive.

CSR and ESG/BRSR are the softer uses. Green credits can support CSR reporting and feed ESG and BRSR disclosure as evidence of a funded restoration commitment. They’re useful for the narrative, but they don’t carry the statutory weight of the afforestation route — and the same credit can’t be claimed twice across them.

What should companies check before funding a project?

If you are funding a project, three things deserve hard scrutiny before any money moves.

- Survival risk is capital risk. The credit depends on trees being alive after five years, and India’s afforestation record here is sobering — performance audits by the Comptroller and Auditor General have found plantation survival rates as low as around 10% in some states. A project that fails to clear 40% canopy returns no credits and no compliance value, only sunk cost. Look closely at the implementing capacity, the species plan, and the monitoring regime.

- Site suitability is not a detail. The rules require a native, site-suitable species mix for a reason: the wrong species on the wrong land is the most common way these projects quietly fail. There is also a deeper question — whether afforesting a particular “degraded” parcel is ecologically sound at all — which we take up in the next article.

- Double-counting is a reputational exposure. If the same trees generating your green credits are also being counted toward carbon credits elsewhere, you may be claiming two environmental benefits from one physical asset. The systemic accounting problem is the next article’s subject; the point for a buyer is narrower and immediate — know exactly what else is being claimed on the land you fund, because the reputational risk lands on you.

Then the practical checks: verifier accreditation and track record, the quality of the Detailed Project Report, force-majeure terms, and — if you are part of a group — whether an intra-group transfer is the cleaner route.

Key definitions

Green credit

A unit issued under the Green Credit Programme for a verified environmental action; for tree plantation, one credit per surviving tree older than five years.

Compensatory afforestation

The statutory afforestation a user agency must carry out to compensate for diverting forest land to non-forest use.

Canopy density

The share of ground covered by tree canopy; the Programme requires a minimum of 40% before credits are issued.

Detailed Project Report (DPR)

The technical and financial plan for a restoration project, vetted by the forest department before approval.

Tripartite MoU

The agreement between applicant, state forest department, and administrator; it grants the applicant no land ownership, lease, or resource rights.

Holding–subsidiary transfer

The only permitted transfer of green credits: between a holding company and its direct subsidiaries.

FAQs

No. Under the revised rules, green credits are non-tradable and non-transferable, except between a holding company and its direct subsidiaries. There is no exchange to purchase them from.

Either by funding a restoration project as the registered applicant and earning credits once it performs, or by receiving them through a holding–subsidiary transfer within their own group.

Yes, but not one-to-one. Under guidelines dated 15 September 2025 (OM No. FC-11/104/2025), afforestation raised over degraded forest land under the Programme can be exchanged toward compensatory afforestation — provided the restored land is two to four times the area being diverted, depending on project type (four times for most private projects). Conditions include a five-hectare minimum parcel, a 25-hectare cumulative minimum, and a ten-year maintenance liability, and site-specific plantation obligations cannot be met this way.

Ten years: a five-year establishment phase the applicant funds and executes, followed by five years of maintenance. Credits are issued only after the five-year period and once 40% canopy density is reached.

No. A credit is single-use and is extinguished once exchanged against an obligation.

Survival risk. Credits depend on trees being alive after five years, and audited survival rates have been as low as around 10% in some states. A project that fails to reach 40% canopy returns no credits and no compliance value.

Sources & Further Reading

- CEEW — Green Credit Programme explainer

- Centre allows green credits as a substitute for compensatory afforestation

- Ecological concerns in India’s Green Credit Programme

- MoEFCC — Compensatory afforestation guidelines, OM No. FC-11/104/2025 (15 Sept 2025)

- MoEFCC — Green Credit Programme (official portal)

- MoEFCC revised Green Credit methodology, 29 Aug 2025 (coverage)

- Mongabay (2/02/2022). [Commentary] Forest restoration: challenges and opportunities for India. Available at: https://india.mongabay.com/2022/02/commentary-forest-restoration-challenges-and-opportunities-for-india/

Join the Conversation

Have you worked out what compensatory afforestation really costs your organisation under the 2025 rules — restored land at two to four times the area you are diverting? Is your team treating green credits as a compliance shortcut, or as the decade-long commitment they turn out to be once you read the fine print? We would like to hear how Indian companies are reading this route: as a workable compliance tool, or one heavier than it first appears. If the information in this blog was helpful, write to us, or share this with a colleague weighing a green credit project this year.

For a structured walk-through of whether a green credit project actually fits the obligation in front of you — and what to pressure-test before any capital goes in — reach out to contact@edhasustainability.com. We are practitioners working across compensatory afforestation, BRSR and ESG disclosure, and LCA-grounded project due diligence.

About the Author

Punnia Viswan is Co-Founder & CEO of Edha Sustainability Solutions LLP, an independent sustainability consultancy operating across India. She holds an M.Sc. in Sustainable Development from the University of Surrey, UK, and brings over a decade of ground-level experience spanning organic certification, agritech research, and regenerative agriculture — before pivoting to ESG advisory. At Edha, she advises companies on ESG reporting across frameworks including BRSR, GRI, and the GHG Protocol; forest restoration and compensatory afforestation strategy; carbon markets and green credit due diligence; and SDG-aligned impact measurement. She has conducted biochar research at London South Bank University and holds UNITAR certifications in Carbon Taxation and REDD+. Edha works with MSMEs, exporters, and local government bodies across India.