The 2026 global SDG scorecard drops in June. Europe’s early edition has already sounded the alarm. Here’s why every Indian business with ESG ambitions or European clients needs to pay attention.

Written by Punnia Viswan | Co-Founder & CEO, Edha Sustainability Solutions LLP | Last updated: 20th May 2026 | All external links verified at time of publication

By the Numbers — SDG 2026 at a Glance

<20% of global SDG targets are on track to be met by 2030 (ESDR 2026, SDSN).

0 European countries on track to achieve all 17 SDGs by 2030 (ESDR 2026).

~40% of EU greenhouse gas emissions are generated abroad through trade — outsourced into global supply chains (SDSN, Feb 2026).

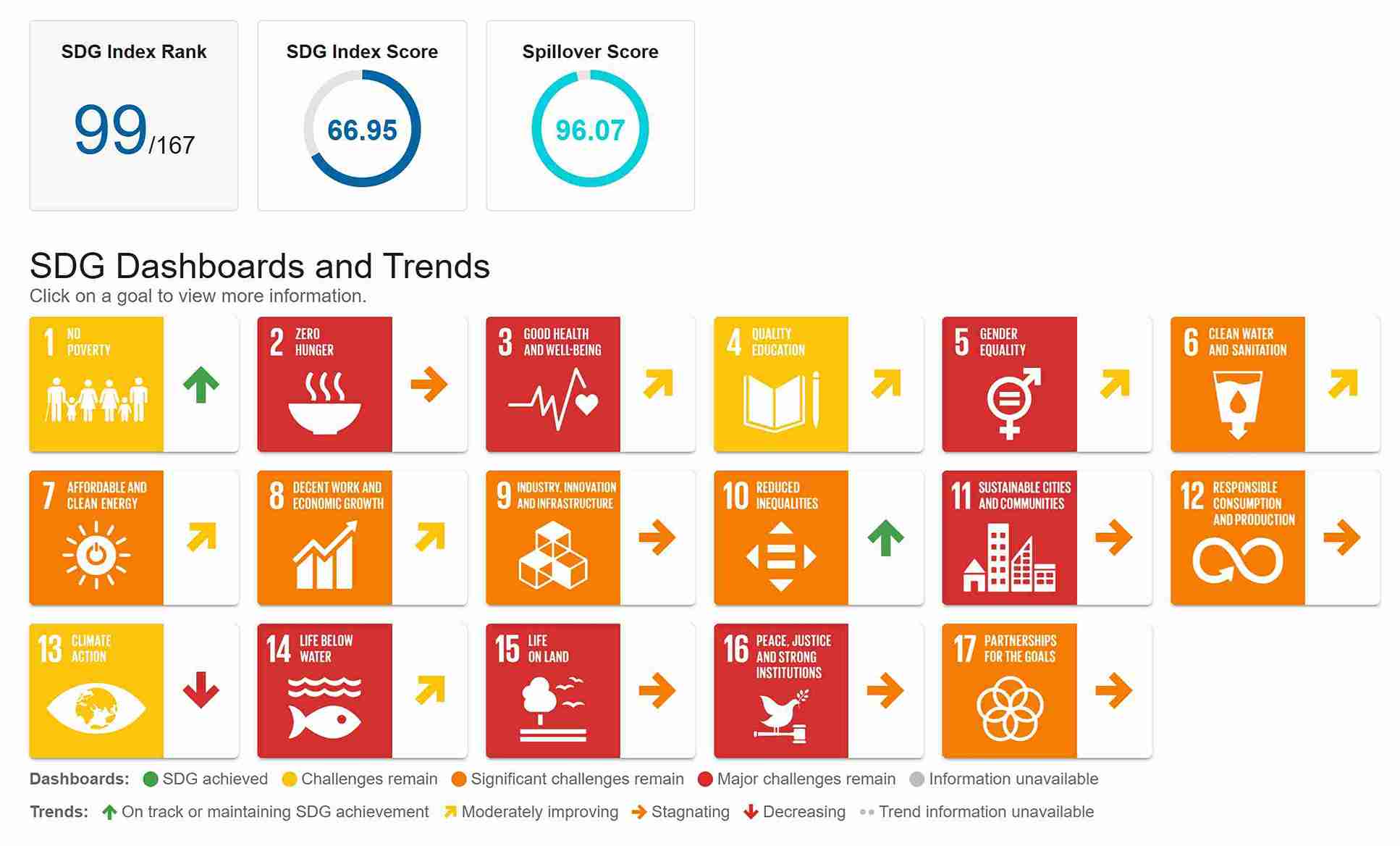

99th India’s SDG rank in SDR 2025 — first-ever entry into the top 100 out of 167 countries, up from 109th in 2024.

₹CBAM Indian steel and aluminium exporters are already paying Carbon Border Adjustment Mechanism charges to the EU (2026).

June 2026 Expected publication date of the global Sustainable Development Report 2026 (SDR 2026)May 7, 2026 SDSN President Prof. Jeffrey D. Sachs signed MoU with IDCA in Rome to align AI & digital infrastructure with SDGs.

Introduction

Here is a number that should stop every Indian CFO and sustainability head in their tracks: fewer than 20% of global SDG targets are on track to be met by 2030. According to the Europe Sustainable Development Report 2026 (ESDR 2026), released by the UN Sustainable Development Solutions Network (SDSN) on 26 February 2026, SDG progress has stalled across all 41 European countries assessed and it is a reliable preview of what the global scorecard, due in June, is almost certain to confirm.

Europe, the region that topped every global sustainability ranking, championed the 2030 Agenda on the world stage, and built the regulatory machinery most Indian exporters are scrambling to comply with has stalled. Not a single European country is on track to achieve all 17 SDGs. Climate action, biodiversity, and responsible consumption are flashing red. And, as the ESDR 2026 documents, approximately 40% of the EU’s greenhouse gas emissions are generated abroad through trade, outsourced invisibly into supply chains that run straight through countries like India.

And yet, this is also an opening. While Europe retreats, India is climbing. According to the SDR 2025, India ranked 99th on the SDG Index for the first time in the top 100 out of 167 countries, up from 109th in 2024. Indian businesses that read the global signals correctly and build credible, verifiable ESG strategies now have a genuine window to differentiate themselves in markets where sustainability credibility is becoming a commercial prerequisite.

In this post, we unpack what the ESDR 2026 tells us, why it matters for Indian businesses specifically, and what practical strategies will separate leaders from laggards before the global scorecard lands in June.

Figure 1: The SDG scorecard of India. Source: SDSN SDG Dashboards – Sustainability Development Report, 2025 (https://dashboards.sdgindex.org/profiles/india/)

Why Is the World Falling Behind on the SDGs?

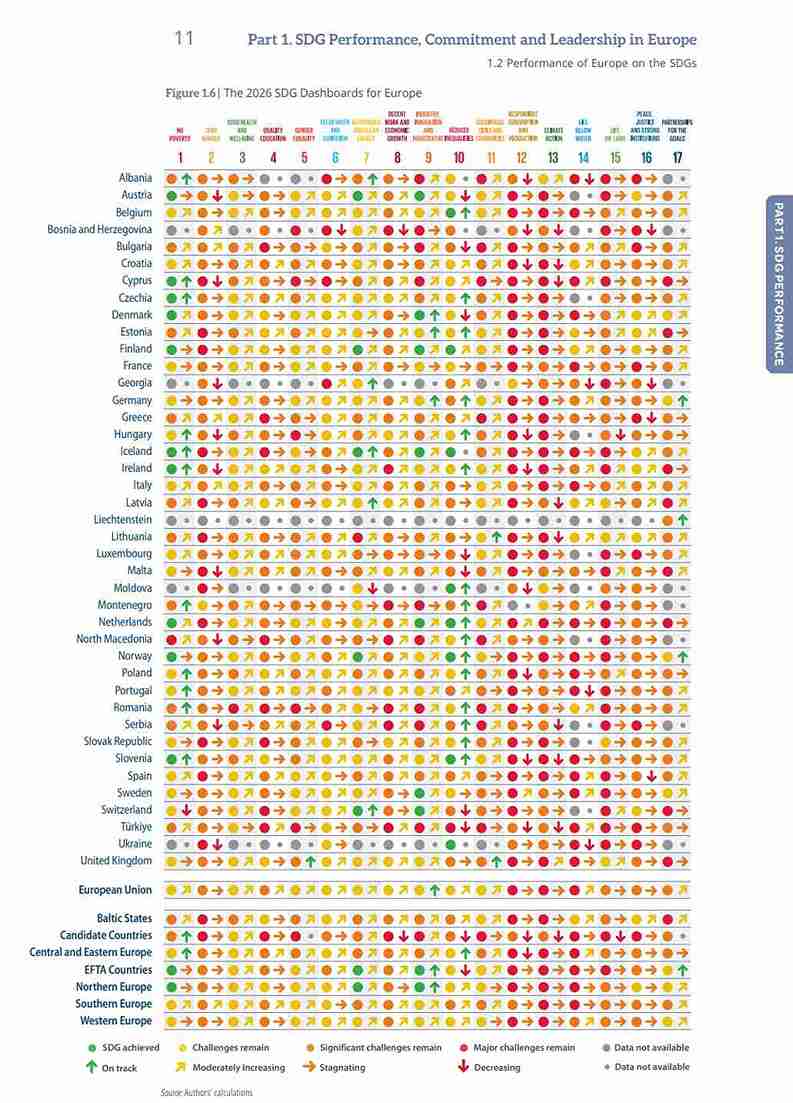

Figure 2: Europe’s 2026 SDG Index — even top-ranked Finland, Sweden, and Denmark face major challenges in at least two SDGs. (Source: ESDR 2026, SDSN)

According to the ESDR 2026, published by SDSN’s SDG Transformation Center in Paris, SDG progress has stalled or reversed on key environmental and socio-economic targets across all 41 countries assessed. The report’s authors, led by Guillaume Lafortune, Vice President of SDSN, and Grayson Fuller, describe it not as a slowdown but as a structural retreat.

The specific SDGs where Europe is struggling matter enormously for Indian businesses because these are the same goals driving European regulatory and procurement pressure on global supply chains:

- SDG 13 — Climate Action: Despite net-zero targets, European GHG reductions are too slow, and the EU’s CBAM mechanism already levies charges on Indian steel and aluminium exports.

- SDG 12 — Responsible Consumption & Production: The EU’s push for product-level sustainability data from the CSRD to Ecodesign Regulation is creating compliance requirements that cascade down to Indian suppliers.

- SDG 14 & 15 — Life Below Water and On Land: European biodiversity failures are translating into tighter supply chain due diligence laws affecting how European companies source from India.

- SDG 2 — Sustainable Agriculture: European agricultural sustainability struggles are reshaping food import standards globally, with consequences for Indian agri-exporters.

The political dimension compounds the problem. According to the ESDR 2026, explicit references to the SDGs and the 2030 Agenda have largely disappeared from European Commission Work Programmes since 2025, replaced by competitiveness, defence, and strategic autonomy (Menon, 2026). Fewer than 40% of citizens in France, Germany, and the UK trust their governments, a political trust deficit that complicates any SDG reform effort.

“With less than five years remaining until 2030, Europe cannot afford complacency. The latest Europe SDR makes it clear that progress on the SDGs is uneven and, in some areas, even reversing.” — Stoyan Tchoukanov, EESC NAT President, February 2026

What this means structurally: the regulatory standards already landing on Indian exporters, CBAM charges, CSRD supply chain disclosure requirements, EUDR deforestation provisions are going to intensify, not relax, regardless of the EU’s political hedging. The regulations are the EU’s response to its own SDG gaps. The wider the gap, the more aggressive the regulatory response.

Meanwhile, on 7 May 2026, SDSN President Professor Jeffrey D. Sachs signed an MoU with the International Data Centre Authority (IDCA) in Rome, formalising a multi-year collaboration to align digital infrastructure such as data centres, compute capacity, and artificial intelligence with the SDGs and the post-2030 agenda. This signals strongly that the global SDR 2026 may introduce an entirely new AI-and-sustainability dimension: how well countries are governing digital technologies in service of their development goals.

Five Strategies Indian Businesses Should Act on Before June 2026

The global SDG picture is sobering. But the story for Indian businesses is not one of helplessness, it is one of strategic timing. Here are five evidence-backed approaches that forward-thinking companies are already using, or should be:

How Should Indian Companies Use BRSR to Build ESG Credibility?

According to SEBI’s BRSR framework, India’s Business Responsibility and Sustainability Reporting requirements are following a clear expansion path. FY 2025–26 mandates BRSR with third-party assurance for the top 500 listed entities; by FY 2026–27, all top 1,000 companies are covered. Critically, the first year of mandatory assurance for the top 250 companies revealed that many self-reported GHG emissions, water, and waste datasets did not survive auditor scrutiny, pointing to systemic gaps in measurement boundary-setting, activity data capture, and calculation methodology.

The strategic move is to treat BRSR data-gathering as the backbone of a live ESG management system, but not a once-a-year compliance sprint. Companies that build real-time data infrastructure now will respond to evolving frameworks (ISSB, GRI, CSRD equivalents) with agility rather than panic.

Pros: Regulatory certainty, investor confidence, audit-ready data.

Cons: Upfront investment in systems and training; cross-functional buy-in required.

How Do You Map Scope 3 Emissions Before Your European Buyers Do It for You?

According to the ESDR 2026, approximately 40% of EU GHG emissions are generated abroad through trade. This means that the European companies are under mounting pressure to account for emissions embedded in their supply chains. The top 250 listed Indian companies are already required to disclose Scope 3 GHG emissions on a comply-or-explain basis under SEBI’s BRSR Core. But the more urgent driver is European buyers, who will increasingly demand verified Scope 3 data as a procurement precondition.

Indian textile exporters certified under GOTS (Global Organic Textile Standard) already disclose chemical use, water consumption, and social compliance. Those layering GHG Protocol–aligned Scope 3 reporting on existing certifications are moving from ‘compliant supplier’ to ‘preferred partner’ in European buyer negotiations.

Pros: Competitive advantage with EU buyers; directly reduces CBAM exposure.

Cons: Complex data collection across supply tiers; expert guidance on methodology required.

How Do You Align an ESG Strategy with India’s SDG Priorities?

Figure 3: India’s SDG progress is uneven — urban sustainability and clean energy show promise, while biodiversity and food systems lag. Smart ESG strategies align materiality with national SDG gaps (illustrative image)

According to the SDR 2025, India ranked 99th globally on the SDG Index, a meaningful improvement, but eight SDGs remain unlikely to be achieved by 2030 without significant acceleration. The SDGs where India struggles most, gender equality, biodiversity, sustainable consumption, are also where ESG disclosure gaps are largest and stakeholder pressure is growing fastest.

Smart companies conduct formal SDG-aligned materiality assessments identifying which of the 17 goals their operations most significantly impact and where they have the greatest opportunity to contribute. This sharpens ESG strategy by focusing resources on areas of genuine materiality and creates a compelling investor narrative that goes beyond compliance.

Pros: Authentic ESG positioning; stronger investor and buyer narrative.

Cons: Requires expert multi-stakeholder facilitation; cannot be credibly done in-house alone.

How Can Indian Businesses Use AI-Enabled Tools for ESG Data?

According to the SDSN–IDCA MoU signed on 7 May 2026 in Rome, the world’s leading SDG monitoring body has committed to integrating AI and digital infrastructure into SDG tracking. The signal for Indian businesses is clear: the next generation of SDG measurement will be AI-assisted, data-intensive, and far more granular. Companies investing now in digital ESG infrastructure such as automated emissions tracking, satellite-backed monitoring, AI-powered supplier audits will meet future reporting standards at a fraction of the cost that reactive companies will face.

Pros: Future-proof reporting; real-time risk monitoring; alignment with SDSN/UN digital frameworks.

Cons: Technology investment costs; data governance protocols must precede automation.

How Does ESG Become a Trade Strategy, Not Just a Reporting Exercise?

Indian steel and aluminium exporters are already paying CBAM charges to the European Union as of 2026. CBAM will expand to chemicals, cement, and hydrogen — and the cost of non-compliance will only grow. According to ESG compliance analysis from Bilancia Group (April 2026), verified, third-party-assured ESG performance is now a trade cost reduction mechanism. Companies that invest in sustainability measurement and certification are not spending on ESG, but they are investing in market access.

Pros: Direct CBAM cost reduction; premium market positioning; supply chain resilience.

Cons: Requires cross-department alignment between finance, operations, and sustainability teams.

What Does SDR 2026 Mean for Specific Indian Sectors?

The implications of the 2026 SDG scorecard are not uniform across Indian industry. Here is how the signals map to specific sectors:

| Sector | SDR 2026 Implication |

| Textiles & Apparel | CSRD supply chain disclosures and GOTS certification gaps make Scope 3 transparency the key differentiator with European buyers. Verified chemical use and social compliance data are increasingly procurement conditions. |

| Steel & Aluminium | CBAM charges are live. Verified carbon accounting is now a direct trade cost reduction mechanism. Companies with low-carbon production and third-party-assured GHG data hold a structural pricing advantage. |

| Construction & Real Estate | C&D Waste Rules 2025 and SDG 11 (Sustainable Cities) create both regulatory urgency and an investor narrative opportunity. IGBC certification and circular economy compliance are increasingly investor-facing signals. |

| Pharma & Chemicals | CBAM expansion to chemicals is on the horizon. EU reach regulations (SVHC, SCIP database) are tightening. Scope 3 and supply chain chemical disclosure are becoming standard buyer expectations. |

| Agri & Food Exports | SDG 2 and SDG 15 failures in Europe are reshaping import standards. The EU Deforestation Regulation (EUDR) requires verifiable traceability for palm oil, soy, and cocoa supply chains touching Indian processors. |

| IT & Digital Services | The SDSN–IDCA MoU signals a new AI-governance-and-SDG dimension in global reporting. Indian IT companies serving European clients will increasingly face questions about data centre energy use, AI ethics, and digital equity. |

What Are the Real Barriers – and Is 2030 Still Achievable?

It would be dishonest to write about ESG strategy without naming the barriers squarely. Here is what makes this hard and why none of these barriers are insurmountable.

The Barriers

- Data scarcity and quality: The first round of mandatory BRSR Core assurance revealed widespread inconsistencies. Most Indian companies are still building the internal data infrastructure that credible ESG reporting demands.

- Capacity gaps in the profession: SEBI’s recalibration in March 2025 from ‘assurance’ to ‘assessment or assurance’ was an acknowledgement that qualified sustainability professionals in India are insufficient to cover 1,000 companies by FY 2026–27.

- Political uncertainty: As the ESDR 2026 shows even in Europe, political commitment to SDGs is fragile. Businesses that build ESG systems for genuine value creation, not just compliance, are more resilient to regulatory reversals.

- Global headwinds: The US has explicitly opposed the SDGs and withdrawn from multilateral frameworks, weakening global momentum and creating confusion for Indian exporters navigating multiple market requirements simultaneously.

The Outlook — and Why Optimism Is Warranted

Notwithstanding the barriers, the trajectory for Indian businesses is genuinely encouraging. According to SDR 2025, India’s improvement from 112th in 2023 to 99th in 2025 is a real signal of momentum, not a statistical anomaly. The mandatory expansion of BRSR is creating a compliance baseline from which genuine ESG leadership can be built. And the SDSN–IDCA partnership, signed just weeks before the global SDR 2026 drops, signals that the global SDG monitoring architecture is being upgraded — making credible ESG data more valuable, not less.

“The SDGs remain our most powerful framework for securing a future that is just, peaceful, and sustainable.” — Guillaume Lafortune, Vice President, SDSN & Lead Author, ESDR 2026

The Scorecard Is Coming — Which Side of It Do You Want to Be On?

When the global SDR 2026 is published in June, it will tell the world, investors, regulators, buyers, and civil society, how far humanity has actually come on its most important promise. Based on the European edition and the global dashboard, the verdict will be uncomfortable reading.

But here is the thing about uncomfortable reading: it tends to accelerate action. The ESG regulatory scaffolding is already in place — BRSR, CBAM charges, CSRD cascades. The AI-and-SDG infrastructure being built through the SDSN–IDCA partnership is going to make sustainability measurement more rigorous and more public than ever before. The 2026 global scorecard will not be the last word — it will be a trigger.

The choice for Indian businesses is not whether to engage with this agenda. That choice has already been made by regulators and markets. The choice is whether to engage strategically, proactively, and early enough to capture the advantage — or reactively, expensively, and late.

The scorecard drops in June. The real question is: which side of it do you want to be on?

Frequently Asked Questions

The Sustainable Development Report 2026 (SDR 2026) is the annual global assessment published by the UN Sustainable Development Solutions Network (SDSN), tracking all 193 UN member states’ progress across the 17 Sustainable Development Goals (SDGs). The global edition is expected in June 2026. An early regional edition — the Europe Sustainable Development Report 2026 (ESDR 2026) — was released on 26 February 2026 and found that SDG progress has stalled across all European countries, with fewer than 20% of global SDG targets on track for 2030. Source: SDSN SDG Transformation Center.

The ESDR 2026, released by the UN SDSN on 26 February 2026, found that SDG progress has stalled across all 41 European countries assessed. No European country is on track to achieve all 17 SDGs by 2030. The report highlights major failures on climate action (SDG 13), biodiversity (SDGs 14 & 15), and responsible consumption (SDG 12). Roughly 40% of EU greenhouse gas emissions are generated abroad through trade. Political commitment to the SDGs has declined, with SDG references removed from European Commission Work Programmes since 2025.

BRSR (Business Responsibility and Sustainability Reporting) is India’s mandatory ESG disclosure framework, regulated by SEBI. As of FY 2025–26, BRSR filing with third-party assurance is mandatory for the top 500 listed companies. By FY 2026–27, all top 1,000 listed companies are covered. The BRSR Core framework requires the top 250 entities to disclose Scope 3 GHG emissions on a comply-or-explain basis.

The EU’s Carbon Border Adjustment Mechanism (CBAM) is a carbon tariff on imports from countries with weaker carbon pricing than the EU. Indian steel and aluminium exporters are already paying CBAM charges as of 2026. CBAM will expand to chemicals, cement, and hydrogen. Companies with verified, low-carbon production hold a structural pricing advantage. For Indian exporters, CBAM makes ESG measurement a trade cost issue, not just a reporting one.

According to the Sustainable Development Report 2025 published by the UN SDSN, India ranked 99th out of 167 countries on the SDG Index with a score of 67 out of 100 — its first-ever entry into the top 100, up from 109th in 2024 and 112th in 2023. Despite this progress, eight SDGs remain unlikely to be achieved by India by 2030 without significant acceleration, particularly in gender equality, biodiversity, and sustainable consumption.

When European SDG progress stalls, regulatory pressure on global supply chains intensifies — because regulations like CBAM, CSRD, and EUDR are the EU’s mechanism for closing its SDG gaps. Indian businesses that export to Europe face cascading disclosure requirements: carbon border charges, supply chain due diligence, and ESG data reporting from European buyers. In practice, Europe’s SDG shortfalls become India’s compliance deadlines.

On 7 May 2026, SDSN President Professor Jeffrey D. Sachs signed an MoU with the International Data Centre Authority (IDCA) in Rome to align digital infrastructure — including data centres, compute capacity, and AI — with the SDGs and the post-2030 agenda. This signals that the SDR 2026 is likely to introduce a new AI-and-sustainability dimension. For Indian businesses investing in digital transformation, this is a forward indicator of how technology governance will be assessed against global sustainability frameworks.

According to the ESDR 2026, all 41 European countries face major challenges in at least two SDGs. The most severely lagging goals are: SDG 13 (Climate Action), SDG 14 (Life Below Water), SDG 15 (Life on Land), SDG 12 (Responsible Consumption & Production), and SDG 2 (Zero Hunger / Sustainable Agriculture). Even top-ranked Finland, Sweden, and Denmark face significant environmental challenges. No European country is on track to achieve all 17 SDGs by 2030.

Scope 3 emissions are indirect GHG emissions across a company’s value chain — from raw material sourcing to product disposal. Under SEBI’s BRSR Core framework, India’s top 250 listed companies must disclose Scope 3 emissions on a comply-or-explain basis from FY 2024–25. For most manufacturing and FMCG companies, over 70% of total emissions sit in the value chain — making Scope 3 the most material and complex disclosure category, and the one European buyers are most urgently demanding data on.

Five evidence-backed strategies are: (1) Treat BRSR as a live ESG management system, not a compliance filing; (2) Map Scope 3 emissions proactively before European buyers require it; (3) Conduct an SDG-aligned materiality assessment; (4) Invest in AI-enabled ESG data infrastructure aligned with the SDSN–IDCA framework; and (5) Position ESG as a trade cost strategy — particularly to reduce CBAM charges. Companies that act before June 2026 will be better placed than those responding after.

Professor Jeffrey D. Sachs is President of the UN Sustainable Development Solutions Network (SDSN), University Professor at Columbia University, and an SDG Advocate for UN Secretary-General António Guterres. He is co-founder of the SDSN (established 2012) and lead co-author of the annual Sustainable Development Report. In May 2026, Sachs signed an MoU with the IDCA in Rome to align global digital infrastructure and AI development with the SDGs — signalling a new technology dimension in SDG monitoring.

ESG reporting refers to disclosing a company’s Environmental, Social, and Governance performance through frameworks like BRSR, GRI, or ISSB. SDG alignment is the broader practice of mapping a company’s strategy and impact against the UN’s 17 Sustainable Development Goals. For Indian businesses, the two are increasingly connected: SEBI’s BRSR explicitly references SDG targets, and international investors increasingly expect companies to show how their ESG performance contributes to national and global SDG progress.

Key Definitions

BRSR (Business Responsibility and Sustainability Reporting)

India’s mandatory corporate ESG disclosure framework, regulated by SEBI. Applies to top 1,000 listed companies by market capitalisation, with progressive assurance requirements phased in from FY 2022–23 to FY 2026–27. Aligns with GRI Standards and references the UN SDGs.

CBAM (Carbon Border Adjustment Mechanism)

A European Union carbon tariff on imports of goods from countries with lower carbon pricing than the EU. Currently applies to steel, aluminium, cement, fertilisers, electricity, and hydrogen. Indian exporters in covered sectors are already paying CBAM charges. Expansion to additional sectors is planned.

CSRD (Corporate Sustainability Reporting Directive)

A European Union directive requiring large companies and listed SMEs to disclose environmental and social information. Creates cascading disclosure obligations down supply chains — including for Indian companies supplying European clients.

ESG (Environmental, Social, and Governance)

A framework for measuring and disclosing a company’s sustainability and ethical performance across three dimensions: environmental impact (emissions, water, waste), social performance (labour, communities, supply chains), and governance (board structure, transparency, accountability).

GRI (Global Reporting Initiative)

The world’s most widely used sustainability reporting framework, providing standards for disclosing environmental, social, and governance performance. SEBI’s BRSR framework draws significantly from GRI Standards.

GHG Protocol

The international accounting standard for quantifying greenhouse gas (GHG) emissions, categorised into Scope 1 (direct emissions), Scope 2 (purchased energy), and Scope 3 (value chain emissions). Underpins BRSR, CSRD, and most ESG frameworks.

ISSB (International Sustainability Standards Board)

A global body established by the IFRS Foundation to develop international sustainability disclosure standards. Its IFRS S1 and IFRS S2 standards are increasingly referenced by regulators worldwide as the baseline for investor-focused ESG disclosure.

SDG (Sustainable Development Goals)

A set of 17 interconnected global goals adopted by 193 UN member states in 2015, forming the 2030 Agenda for Sustainable Development. Span poverty, health, education, climate action, biodiversity, and institutional governance. Progress is tracked annually by the UN SDSN through the Sustainable Development Report.

SDR (Sustainable Development Report)

The annual global assessment of SDG progress published by the UN SDSN, ranking all 193 UN member states. The SDR 2026 global edition is expected in June 2026. A regional Europe edition (ESDR 2026) was released on 26 February 2026.

SDSN (UN Sustainable Development Solutions Network)

Established in 2012 under the auspices of the UN Secretary-General, the SDSN mobilises over 2,000 universities, research centres, and think tanks across 150 countries to advance the SDGs. It publishes the annual Sustainable Development Report. SDSN President is Professor Jeffrey D. Sachs.

Scope 3 Emissions

Indirect greenhouse gas emissions that occur across a company’s full value chain — upstream (raw materials, logistics, suppliers) and downstream (product use, end-of-life disposal). For most manufacturing and FMCG companies, Scope 3 accounts for over 70% of total GHG footprint.

Sources & Further Reading

- Bilancia Group. ‘ESG Compliance in 2026: Key regulatory changes every Indian business must know, April 24 2026

- Drishti The Vision Foundation. 25 June 2025. Daily Updates. 10th Sustainable Development Report 2025. Available at: https://www.drishtiias.com/daily-updates/daily-news-analysis/10th-sustainable-development-report-2025

- ESG 360. BRSR core expansion: Value chain partner reporting from FY 2025-26 – What Indian companies must start preparing for now. Available at: https://esg360.in/2026/01/23/brsr-core-expansion-value-chain-partner-reporting-from-fy-2025-26-what-indian-companies-must-start-preparing-for-now/

- Europe Sustainable Development Report 2026 (ESDR 2026), SDSN SDG Transformation Center, February 25 2026

- HECS. 28 July 2025. Decoding ESG for Indian Industries: What it means and how to start. Available at: https://hecs.in/esg-for-indian-industries

- Menon, N. 27 February 2026. ‘Europe sustainable development report flags climate, Inequality gaps in EU’. ESG Times. Available at: https://www.esgtimes.in/esg/sustainability/europe-sustainable-development-report-flags-climate-inequality-gaps-across-eu/

- SDG Dashboards — Country Rankings & Interactive Maps, SDSN, 2025

- SDG Transformation Center. IDCA and the SDSN sign MoU in Rome to align digital infrastructure with the Global Sustainability Agenda. May 7, 2026, Rome, Italy. Available at: https://sdgtransformationcenter.org/news/idca-sdsn-mou-rome

- SDR 2025 Public Consultation — Global Scorecard Preview, SDSN, 2026

- SDSN–IDCA MoU: Aligning Digital Infrastructure with SDGs, May 8, 2026

Join the Conversation

Is your organisation already mapping its SDG exposure? Have CBAM charges or CSRD cascades started showing up in your supply chain conversations? We would love to hear how Indian businesses are navigating this — drop your experience in the comments, or share this post with a colleague who needs to see the numbers. The global SDR 2026 lands in June. Let us talk about it before — and after — it does.

For a structured walk-through of what the SDR 2026 means specifically for your sector or ESG disclosure stage, reach out to Edha Sustainability Solutions LLP — we are practitioners working across BRSR, GRI, CBAM readiness, and SDG-aligned impact measurement.

About the Author

Punnia Viswan is Co-Founder & CEO of Edha Sustainability Solutions LLP, an independent sustainability consultancy operating across India. She holds an M.Sc. in Sustainable Development from the University of Surrey, UK, and brings over a decade of ground-level experience spanning organic certification, agritech research, and regenerative agriculture — before pivoting to ESG advisory. At Edha, she specialises in ESG reporting across frameworks including BRSR, GRI, and the GHG Protocol; sustainability certifications such as GOTS and IGBC; circular economy advisory; and SDG-aligned impact measurement. She has conducted biochar research at London South Bank University and holds UNITAR certifications in Carbon Taxation and REDD+. Edha works with MSMEs, exporters, and local government bodies across India.